ASEAN Investment: Thailand’s Growing EV Market as a Regional Hub

As the center of ASEAN automobile production, Thailand is leveraging its automotive supply chain to become a regional hub for electric vehicle (EV) production. With motorcycles accounting for most of the transportation modes, EV adoption is on the rise, and the passenger car sector is expected to reach a 10% market penetration rate by September 2023. Though EV trucks initially faced challenges, global sustainability trends are expected to drive increased adoption in Thailand’s logistics sector. As the Thai government extends EV support policies beyond Bangkok, the automotive sector is expected to continue evolving.

This article delves into Thailand’s EV market, current trends, and future outlook.

Thailand’s EV Segments

Electric Two-Wheelers (E2W)

While electric two-wheelers (E2W) account for only 0.1% of Thailand’s 22.6 million motorcycles, the market has seen impressive growth, with a compound annual growth rate (CAGR) of 150% from 2020 to 2022. EV two-wheeler sales reached 9,886 units in 2022, achieving a penetration rate of about 0.5% in an annual market of 1.8 million units. Key players include Deco Co. (29% market share) and H SEM Co. (16%). Notably, AJ EV Bike experienced over 400% growth in the first three quarters of 2023, positioning it as a brand to watch. Major corporations, such as 7-Eleven, have strategically adopted EV scooters for significant cost savings and environmental benefits.

As part of its EV roadmap, “30@30,” the Thai government aims to produce 675,000 electric two-wheelers (E2W) annually by 2030. Currently, EV bike batteries are sourced both locally and through imports; however, partnerships such as those between PTT and KYMCO indicate a strengthening of local production capabilities. To support this initiative, the Thai government is offering a minimum three-year exemption from corporate income tax (CIT) for EV bike battery manufacturers and may consider additional tax exemptions in the future.

Source: Thailand Land Transport Department

Source: Thailand Land Transport Department

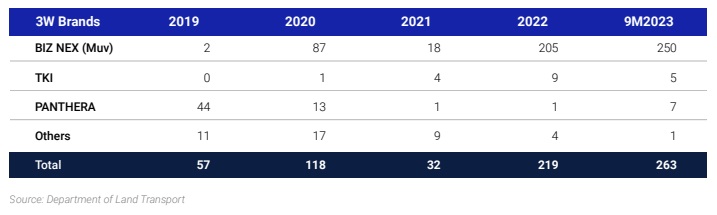

Electric Three-Wheelers (E3W)

The electric three-wheeler (E3W) market in Thailand is experiencing robust growth, especially with the iconic “Tuk-Tuk.” Between 2022 and September 2023, EV three-wheelers increased by 49%, with around 761 EV three-wheelers currently operating in Thailand. This rapid expansion is driven by MuvMi, Thailand’s first electric Tuk-Tuk ride-sharing service. MuvMi aims to expand its fleet from 350 to 1,000 units in 2023 and reach 5,000 units by 2028 through its partnership with Biz Next Motor Company. Legal frameworks to streamline Tuk-Tuk registration are seen as crucial for further growth. Over 50% of Tuk-Tuks and nearly all E3Ws are concentrated in Bangkok, with Biz Next holding a commanding 94% market share in 2022. Other major players include TKI, Sumota, Panthera, and KYBURZ, which collectively contribute to Thailand’s E3W market expansion, playing a pivotal role in future urban transportation.

Electric Four-Wheelers (E4W)

The fastest-growing segment in Thailand’s EV market is electric four-wheel (E4W) passenger cars, with new vehicle sales surpassing 50,000 units and recording a 400% increase by September 2023. Chinese BEV brands like BYD, Neta, and MG dominate Thailand’s EV market, capturing over 70% of the market share in 2023. Investments in EV components, particularly batteries, are strengthening Thailand’s competitive edge in the BEV market. With strategic location, aggressive policies, and infrastructure investment, Thailand is poised to play an essential role in the expanding EV market.

The E4W market is divided into three segments: affordable, standard, and premium price ranges. In the affordable segment, Chinese manufacturers account for over 75% of sales. However, competition is intensifying within Thailand’s E4W sector, with more brands investing in local production facilities. The Thai government’s EV tax reductions and subsidies for battery manufacturers aim to strengthen the EV supply chain, reduce reliance on imports, and make EVs more accessible and affordable for consumers. Ultimately, the goal is to establish Thailand as a hub for EV production in Southeast Asia.

Source: Thailand Land Transport Department

Source: Thailand Land Transport Department

Source: Thailand Land Transport Department

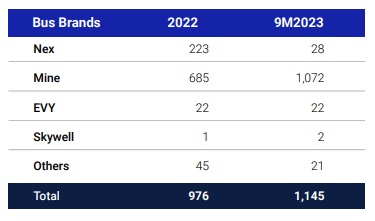

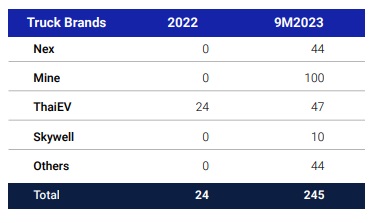

Electric Commercial Vehicles (Buses and Trucks)

Between 2022 and September 2023, EV bus registrations in Thailand increased by 17% to 1,145 units, while EV truck registrations grew 920% to 245 units, marking substantial growth in the large commercial EV segment. The brand “MINE Mobility” leads the market, capturing 96% of the EV bus and 59% of the EV truck markets. Light commercial trucks, especially for last-mile delivery, are seeing increased demand. Challenges around payload capacity, driving range, and charging infrastructure for long-haul use remain, but the market is growing, with 271 EV trucks operational as of September 2023. With rising demand for commercial EVs, local production expansion is anticipated in Thailand.

Expanding Charging Infrastructure

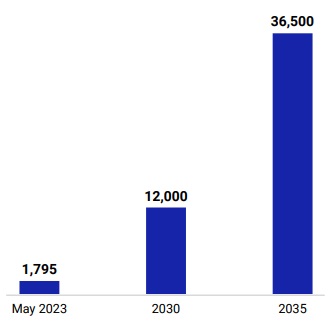

Thailand’s EV charging infrastructure is advancing with government support and private investment. As of September 2023, Thailand has 4,806 AC chargers and 3,896 DC fast chargers installed. The number of DC chargers is expected to continue growing, with the National EV Policy Committee targeting 12,000 DC chargers by 2030 and 36,500 by 2035. The current EV-to-DC charger ratio still needs improvement, requiring an upgraded infrastructure network to support the growing EV population.

In collaboration with INNOPOWER, Siam Commercial Bank has introduced an “EV Home Model” to support homeowners and retailers in setting up EV charging stations. Battery swap services are gaining popularity but face standardization challenges. The Thai government aims to establish 1,450 battery swap stations by 2030 and is conducting research to develop a standardized battery pack for EV bikes. Regional cooperation will be essential to address issues such as standardization, product differentiation, and disparities in battery pack standards across regions. For larger commercial vehicles, especially buses and trucks, challenges related to space limitations and high power requirements for charging infrastructure need to be addressed. As Thailand’s EV market matures, charging infrastructure development is becoming a priority.

While Thailand’s charging stations depend on the national power grid, smart grid technology to optimize electricity generation, transmission, and distribution is still in its early stages. Current projects focus on integrating energy management, solar power, and battery energy storage systems (BESS). The adoption of smart grid technology requires substantial investment, and government support along with industry collaboration is critical to overcome the challenges of solar power limitations and high investment costs.

Source: YCP Solidiance, Dominating SEA’s EV Revolution: The Ultimate Guide to Thailand’s EV Market

Summary

Thailand’s steady growth and alignment in the electric vehicle (EV) industry are evident. The Thai government is actively pursuing the goal of becoming a regional hub for the EV industry by fostering strategic partnerships within the industry and expanding charging infrastructure. As a key player in ASEAN’s EV advancement, Thailand still faces challenges, yet the market’s growth promises valuable business strategies and investment opportunities.

Source: YCP Solidiance, “Dominating SEA’s EV Revolution: The Ultimate Guide to the EV Market in Thailand,” December 2023